import sys, numpy as np, matplotlib.pyplot as plt

sys.path.insert(0,'..')

from engine import ch02

from dataclasses import replaceMFAA Chapter 2 Laboratory

Stochastic Process and Cash-Flow Simulator (book §2.9)

Simulates the drivers of §2.5, assembles cash-flow processes by decomposition (2.3), and makes the two-filtration distinction visible. No valuation yet — cash flows are shown undiscounted. Seed 20260200.

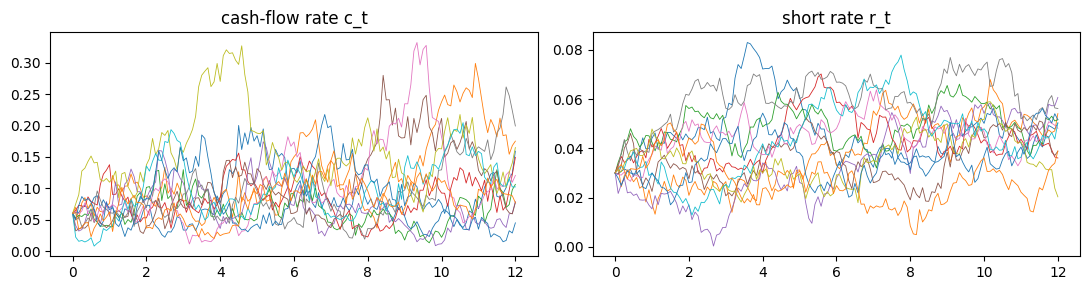

1. Drivers and cash-flow paths

p = ch02.template('buyout')

dr = ch02.simulate_drivers(replace(p, M=2000))

fig,ax = plt.subplots(1,2,figsize=(11,3))

for j in range(12):

ax[0].plot(dr['tgrid'], dr['c'][:,j], lw=.6)

ax[1].plot(dr['tgrid'], dr['r'][:,j], lw=.6)

ax[0].set_title('cash-flow rate c_t'); ax[1].set_title('short rate r_t'); plt.tight_layout()

2. E1 — Scheme error (Euler vs exact; Theorem 2.8.1 slopes ≈ ½ and ≈ 1)

cv = ch02.convergence_diagnostics(ch02.SimParams())

for r in cv['rows']:

print(f"dt {r['dt']:.5f} strong {r['strong_error']:.5f} weak {r['weak_error']:.6f}")

print(f"strong slope {cv['strong_slope']:.3f}, weak slope {cv['weak_slope']:.3f}")dt 0.25000 strong 0.00506 weak 0.000169

dt 0.08333 strong 0.00219 weak 0.000027

dt 0.01923 strong 0.00090 weak 0.000034

dt 0.00397 strong 0.00039 weak 0.000003

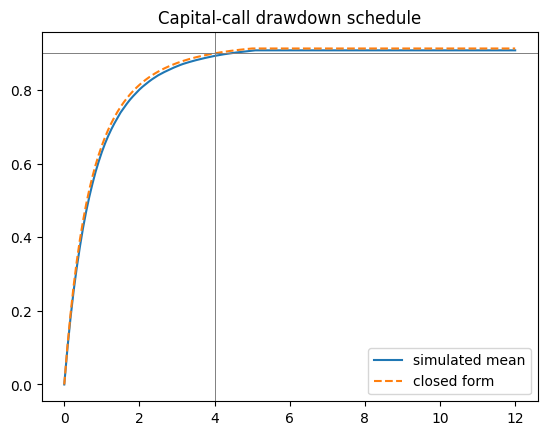

strong slope 0.615, weak slope 0.8593. E2 — Intensity shape: the capital-call drawdown (Exercise 2.10)

Calibrate the age profile so expected cumulative calls reach 90% by year 4.

p = ch02.SimParams(theta=0.5, mark_a=2.0, mark_b=3.0)

lam = ch02.calibrate_lambda_call(p)

print(f'calibrated lam_call = {lam:.4f} (book ≈ 3.33)')

dd = ch02.simulate_drawdown(replace(p, lam_call=lam, M=20000))

i4 = int(round(4/p.dt))

print(f"called-by-year-4: sim {dd['mean_sim'][i4]:.4f} closed {dd['mean_closed'][i4]:.4f}")

plt.plot(dd['tgrid'], dd['mean_sim'], label='simulated mean')

plt.plot(dd['tgrid'], dd['mean_closed'], '--', label='closed form')

plt.axhline(.9, color='grey', lw=.7); plt.axvline(4, color='grey', lw=.7)

plt.legend(); plt.title('Capital-call drawdown schedule');calibrated lam_call = 3.3287 (book ≈ 3.33)

called-by-year-4: sim 0.8930 closed 0.9000

4. E3 — Two filtrations (Exercise 2.11)

The target table: volatility ratio {0, 0.333, 0.500, 0.655, 0.816}, lag-1 autocorrelation {·, 0.8, 0.6, 0.4, 0.2}.

import pandas as pd

pd.DataFrame(ch02.two_filtration_table())| alpha | vol_ratio_sample | vol_ratio_theory | rho1_sample | rho1_theory | |

|---|---|---|---|---|---|

| 0 | 0.0 | 0.000000 | 0.000000 | NaN | NaN |

| 1 | 0.2 | 0.338568 | 0.333333 | 0.806767 | 0.8 |

| 2 | 0.4 | 0.503584 | 0.500000 | 0.607492 | 0.6 |

| 3 | 0.6 | 0.656521 | 0.654654 | 0.405911 | 0.4 |

| 4 | 0.8 | 0.817247 | 0.816497 | 0.204372 | 0.2 |

The committee’s two volatility numbers from the opening problem are two points on the first row of this table — not two estimates of one quantity.

5. Validation checks

v = ch02.validation_checks()

for k,d in v.items():

if isinstance(d,dict): print(k, 'PASS' if d['pass_'] else 'FAIL')

print('ALL:', v['all_pass'])V1_poisson PASS

V2_ou_stationary PASS

V3_cir_stationary PASS

V4_reproducible PASS

ALL: True