import sys, numpy as np, matplotlib.pyplot as plt

sys.path.insert(0,'..')

from engine import ch04

from dataclasses import replaceMFAA Chapter 4 Laboratory

Stochastic DCF Engine (book §4.9)

The book’s first full valuation engine: LDCF operator of Theorem 4.8, premium location, regimes, Bayesian parameter uncertainty. Designed as a hurdle-rate autopsy. Seed 20260400.

1. E1 — Hurdle autopsy

Enter a flat 12% and see what the point estimate was hiding.

p = ch04.DCFParams()

au = ch04.hurdle_autopsy(p)

print(f"flat 12% deterministic value: {au['flat_value']:.4f}")

print(f"full-model mean: {au['full']['mean']:.4f} ± {au['full']['se']:.4f}")

print(f"implied honest flat rate: {au['implied']['implied_flat_rate']:.4f}")

import pandas as pd

pd.DataFrame(au['decomposition'])flat 12% deterministic value: 0.9554

full-model mean: 1.1504 ± 0.0028

implied honest flat rate: 0.0758| stage | mean | se | std | quantiles | |

|---|---|---|---|---|---|

| 0 | deterministic DCF | 1.403467 | 1.570132e-18 | 2.220502e-16 | {'q05': 1.4034674333159036, 'q25': 1.403467433... |

| 1 | + rate risk | 1.247307 | 1.684262e-03 | 2.381906e-01 | {'q05': 0.8632866286499349, 'q25': 1.046989656... |

| 2 | + price-of-risk wedges | 1.154518 | 2.512370e-03 | 3.553028e-01 | {'q05': 0.7591024275595836, 'q25': 0.900515645... |

| 3 | + liquidity friction/factor | 1.150428 | 2.840822e-03 | 4.017529e-01 | {'q05': 0.7194574347974299, 'q25': 0.875777502... |

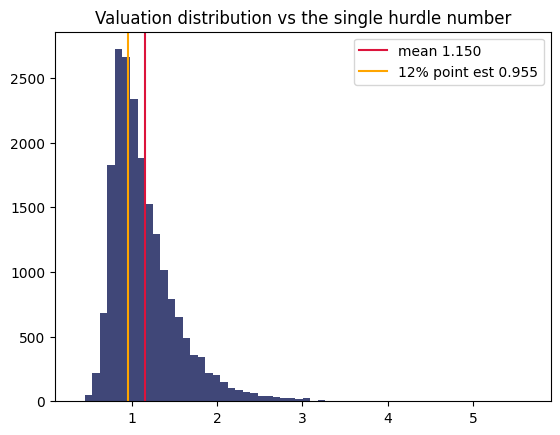

2. The valuation distribution the hurdle was hiding

from engine.ch04 import _simulate_value

v = _simulate_value(p, 'full')

plt.hist(v, bins=60, color='#1E2761', alpha=.85)

plt.axvline(v.mean(), color='crimson', label=f'mean {v.mean():.3f}')

plt.axvline(au['flat_value'], color='orange', label=f"12% point est {au['flat_value']:.3f}")

plt.legend(); plt.title('Valuation distribution vs the single hurdle number');

3. E2 — Double-count demonstration

The single most opinion-changing exercise in Part II: value illiquidity once as a factor in M, once as a friction in the operator, then force both on.

dc = ch04.double_count_check(p)

print(f"factor-in-M: {dc['factor_in_M']['mean']:.4f}")

print(f"friction-in-operator: {dc['friction_in_operator']['mean']:.4f}")

print(f"both active (bug): {dc['both_active']['mean']:.4f}")

print(f"double-count bias: {dc['double_count_bias_vs_factor']:.4f}")factor-in-M: 1.1504

friction-in-operator: 1.1324

both active (bug): 1.1324

double-count bias: -0.01804. E4 — Learning curve (Bayesian panel, Proposition 4.7)

Feed deal outcomes one at a time; watch the posterior premium spread shrink.

bu = ch04.bayesian_update(0.03, 0.02, 0.05, [0.05,0.01,0.04,0.02,0.06,0.03,0.045])

for n,(mn,sd) in enumerate(zip(bu['posterior_mean'], bu['posterior_sd']),1):

print(f"n={n}: posterior {mn:.4f} ± {sd:.4f}")

print('recursion matches batch:', bu['recursion_matches_batch'])n=1: posterior 0.0328 ± 0.0186

n=2: posterior 0.0300 ± 0.0174

n=3: posterior 0.0311 ± 0.0164

n=4: posterior 0.0300 ± 0.0156

n=5: posterior 0.0327 ± 0.0149

n=6: posterior 0.0324 ± 0.0143

n=7: posterior 0.0334 ± 0.0137

recursion matches batch: True5. Zero-coupon curve (closed form vs Monte Carlo) and validation

mats=[1,2,3,5,7,10]

cf=ch04.zcb_closed_form(p,mats); mc=ch04.zcb_monte_carlo(replace(p,M=40000),mats)

for i,T in enumerate(mats): print(f"T={T:2d} closed {cf[i]:.5f} MC {mc['price'][i]:.5f} ± {mc['se'][i]:.5f}")

v = ch04.validation_checks()

print('\nvalidation ALL:', v['all_pass'])T= 1 closed 0.96947 MC 0.96941 ± 0.00003

T= 2 closed 0.93841 MC 0.93826 ± 0.00007

T= 3 closed 0.90738 MC 0.90714 ± 0.00011

T= 5 closed 0.84674 MC 0.84653 ± 0.00019

T= 7 closed 0.78902 MC 0.78877 ± 0.00024

T=10 closed 0.70890 MC 0.70868 ± 0.00030

validation ALL: True