import sys, numpy as np, matplotlib.pyplot as plt

sys.path.insert(0,'..')

from engine import ch09

from dataclasses import replaceMFAA Chapter 9 Laboratory

LBO Valuation Engine (book §9.9)

The opening problem’s spreadsheet, rebuilt with distributions: buyout equity under EBITDA risk, multiple regimes, sweep-driven debt, and optimal exit. Organizing display: the committee panel. Seed 20260900.

1. E1 — Answer the committee

The deterministic base case sits at some percentile of the actual IRR distribution.

p = ch09.LBOParams(M=10000)

panel = ch09.committee_panel(p)

print(f"base-case IRR (deterministic): {panel['base_case_irr']:.4f}")

print(f"mean IRR: {panel['mean_irr']:.4f}, median IRR: {panel['median_irr']:.4f}")

print(f"impairment probability: {panel['impairment_prob']:.3f}")

print(f"the 'base case' sits at percentile {panel['base_percentile']:.2f} of the distribution")

print('IRR quantiles:', {k:round(v,4) for k,v in panel['irr_quantiles'].items()})base-case IRR (deterministic): 0.1473

mean IRR: 0.0960, median IRR: 0.0926

impairment probability: 0.335

the 'base case' sits at percentile 0.61 of the distribution

IRR quantiles: {'q05': -1.0, 'q25': -0.0653, 'q50': 0.0926, 'q75': 0.2214, 'q95': 0.3896}2. E2 — The leverage frontier

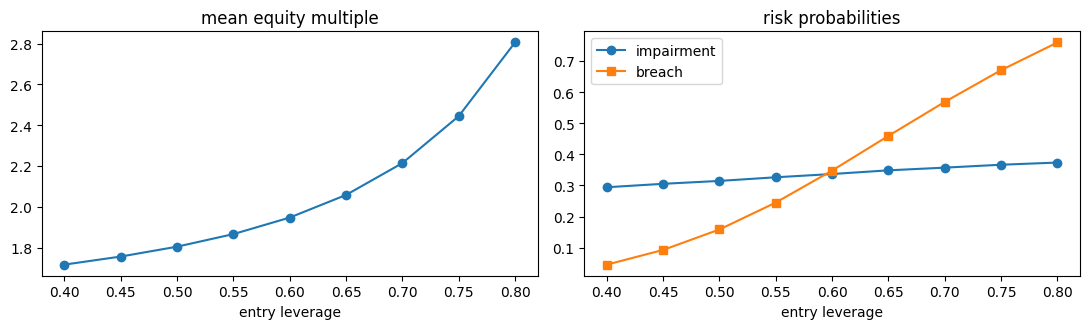

Where do the GP and LP optima diverge?

import pandas as pd

front = ch09.leverage_frontier(ch09.LBOParams(M=6000))

df = pd.DataFrame(front)

fig,ax=plt.subplots(1,2,figsize=(11,3.4))

ax[0].plot(df['leverage'], df['mean_multiple'],'o-'); ax[0].set_title('mean equity multiple'); ax[0].set_xlabel('entry leverage')

ax[1].plot(df['leverage'], df['impairment_prob'],'o-',label='impairment'); ax[1].plot(df['leverage'], df['breach_prob'],'s-',label='breach'); ax[1].legend(); ax[1].set_title('risk probabilities'); ax[1].set_xlabel('entry leverage')

plt.tight_layout(); df| leverage | mean_multiple | impairment_prob | breach_prob | mean_irr | |

|---|---|---|---|---|---|

| 0 | 0.40 | 1.716328 | 0.294167 | 0.045500 | 0.075537 |

| 1 | 0.45 | 1.755869 | 0.305167 | 0.092667 | 0.076394 |

| 2 | 0.50 | 1.804289 | 0.314500 | 0.158500 | 0.078899 |

| 3 | 0.55 | 1.865950 | 0.326167 | 0.245000 | 0.084504 |

| 4 | 0.60 | 1.947023 | 0.336667 | 0.347833 | 0.094614 |

| 5 | 0.65 | 2.057909 | 0.348500 | 0.459333 | 0.112302 |

| 6 | 0.70 | 2.214107 | 0.357167 | 0.568500 | 0.133690 |

| 7 | 0.75 | 2.444144 | 0.366500 | 0.670500 | 0.161995 |

| 8 | 0.80 | 2.805829 | 0.373500 | 0.759500 | 0.207519 |

3. Closed-form validation (Proposition 9.3, lognormal limit)

b = ch09.lognormal_benchmark(ch09.LBOParams(sweep=0, mult_hot=9.75, mult_cold=9.75, regime_rate=0))

print(f"closed-form equity (BS call on EV): {b['closed_form_equity']:.2f}")

v = ch09.validation_checks()

for k,d in v.items():

if isinstance(d,dict): print(k, 'PASS' if d['pass_'] else 'FAIL')

print('ALL:', v['all_pass'])closed-form equity (BS call on EV): 659.88

V1_lognormal PASS

V2_deterministic PASS

V3_leverage_monotone PASS

V4_timing_value PASS

V5_reproducible PASS

ALL: True